Life of a Bubble: How did the global economic crisis

happen?

Key word: fed reserve, housing bubble, trade

deficit

1 Intro

Today I am going to talk about the life of a bubble. It's not just any bubble, it's the biggest one in the past 70 years if not the biggest one in human history. Most of the data came from US census, and the individual testimonies were excerpted from the

NPR special report on the credit crisis, originally aired on May 9, 2008

2 Global Pool of Money doubles

from 35 Trillion in 2001 to 70 Trillion 2007

2.1 Poor countrys getting rich

By making TVs and selling oil: China,

India, Saudi Arabia. Made a lot of money and banked it. China, for example, has

over a trillion dollars in its central bank, and there are office buildings in

Beijing filled with math geniuses-real math geniuses-looking for a place to

invest it. And the world was not ready for all this money. There's twice as

much money looking for investments, but there are not twice as many good

investments. So, that global army of investment managers was hungrier and

twitchier than ever before. They all wanted the same thing: a nice low risk

investment that paid some return.

Incidentally the US trade

deficit also doubled from 2001 to 2007

2001 -365.126 billion

2002 -423.725 billion

2003 -496.915 billion

2004 -607.730 billion

2005 -711.567 billion

2006 -753.283 billion

2007 -700.258 billion

2.2 Greenspan: Reduce The Fed

Funds Rate: From 6.6% in Jan 2001 to 1%

in July 2003

3 mortgage backed securities:

Mike Francis. During the beginning of the mortgage implosion, I was an

executive director at Morgan Stanley on the residential mortgage trading desk.

3.1 Think how attractive a

mortgage loan is to that 70 trillion dollar pool of money. Remember, they're

desperate to get any kind of interest return. They want to beat that miserable

1 percent interest Greenspan is offering them. And here are these homeowners,

they're paying 5, 7, 9 percent to borrow money from some bank. So what if the

global pool could get in on that action? There are problems. Individual

mortgages are too big a hassle for the global pool of money. They don't want

get mixed up with actual people and their catastrophic health problems or

debilitating divorces, and all the reasons which might stop them from paying

their mortgages.So what Mike and his peers on Wall Street did, was to figure

out how to give the global pool of money all the benefits of a mortgage –

basically higher yield - without the hassle or the risk. So picture the whole

chain. Home buyer gets a mortgage from a broker. The broker sells the mortgage

to a small bank, the small bank sells the mortgage to Mike in a big investment

firm on Wall Street. Then Mike takes a few thousand mortgages he’s bought this

way, he puts them in one big pile. Now he’s got thousands of mortgage checks

coming to him every month. It’s a huge monthly stream of money, which is

expected to come in for the next thirty years, the life of a mortgage. And he

then sells shares of that monthly income to investors. Those shares are called

mortgage backed securities. And the 70 trillion dollar global pool of money

loved them.

4 Drive the need for more

mortgage: lower the bar

And in the beginning, he'd

only buy mortgages that were pretty standard and pretty safe. Mortgages where

people had come up with a down payment and proven they had a steady income and

money in the bank.

And they sold so many

mortgages that there came a point in 2003 where just about

everybody who wanted a mortgage and was qualified

to get one .... had gotten one. But

the pool of money had just gotten started. They wanted more mortgage backed

securities.

So Wall Street had to find

more people to take out mortgages. Which meant lending

to people who never would’ve qualified before.

And so Mike noticed that

every month, the guidelines were getting a little looser.

Something called a stated income, verified asset

loan came out, which meant you didn't

have to provide paycheck stubs and w-2 forms, as they had in the past. You

could simply state your income, as long as you showed that you had money in the

bank.

Mike Garner: The next

guideline lower is just stated income, stated assets. Then you state what you

make and state what’s in your bank account.

They call and make sure

you work where you say you work. Then an accountant has to say for your field

it is possible to make what you said you make. But they don’t say what you

make, just say it’s possible that they could make that.

It’s just so funny that

instead of just asking people to prove what they make there’s this theater in place of you

have to find an accountant

sitting right in front of me who could very easily provide a W2, but we’re not

asking for a W2 form, but we do want this accountant to say yeah, what they’re

saying is plausible in some universe.

Loan officers would have

an accountant they could call up

and say “Can you write a statement saying a truck driver can make this much

money?” Then the next one, came along, and it was no income, verified assets.

So you don't have to tell the people what you do for a living. All you have to

do is state you have

a certain amount of money in your bank account. And then, the next one, is just

no income, no asset. You don't have to state anything. Just have to have a

credit score and a pulse.

Actually that pulse thing

is also optional. Like the case in Ohio where 23 dead people were approved for mortgages.

5 Housing bubble

It's easy to ignore your

gut fear when you are making a fortune in commissions. But Mike had other help in

rationalizing what he was doing.

Technological help. Mike

sat at a desk with six computer screens, connected to millions of dollars worth

of fancy analytic software designed by brilliant Ivy league math geniuses hired

by his firm, which analyzed all the loans in all the pools that he bought and

then sold. And the software, the data ... didn’t seem worried at all:

Mike Francis:

"All the data that we

had to review, to look at, on loans in production that were years old, was

positive. They performed very well. All those factors, when you look at the

pieces and parts. A 90% NINA loan from 3 years ago is performing amazingly

well. Has a little bit of risk. Instead of defaulting 1.5% of the time it

defaults at 3.5% of the time. That’s not so bad. If I’m an investor buying

that, if I get a little bit of return, I’m fine.

"

As we now know, they were

using the wrong data. They looked at the recent history of mortgages and saw

that foreclosure rate is generally below 2 percent. So they figured, absolute

worst-case scenario, the foreclosure rate may go to 8 or 10 or 12 percent. But

the problem with is there were all these new kinds of mortgages, given out to

people who never would have gotten them before. So the historical data was

irrelevant. Some mortgage pools, today, are expected to go beyond 50 percent

foreclosure rates.

That explains why the

mortgage backed security seems to perform well at the beginning of the bubble.

Why did it continue to perform will after the initial 3 years?

The answer is home equity

lines of credit, or HELOC.

Through HELOC, the home

owners could take out another loan from the bank, against the value of their

house, which had increased because of the bubble. HELOC became very popular

between 2003 and 2006, partly because they were easy to get; partly because

people needed them to continue making their original mortgage payments.

To pay off their debts,

they went into more debt.

5.1 A big part of this story,

of this whole crisis, is that a lot of really smart people, people who knew

better, fooled themselves with this data. It was the triumph of data over common

sense.

6 The thing that took this

problem and turned it into a crisis was something else that was new, something

called a Collateralized Debt Obligation, CDO

6.1 A mortgage-backed security,

you remember, is a pool of thousands of different mortgages. These are all put

together and divided into different slices. Some of these slices are risky,

some are not. OK, a CDO is a pool of those slices. A pool of pools.

There's another term the

industry uses, no joke, they call these lower-rated tranches toxic waste.

They're so high-risk, they're toxic.

So, a CDO is sort of a

financial alchemy. Jim takes that toxic stuff, these low- rated, high-risk

tranches, puts them all together. Re-tranches them, and presto: he has a CDO

whose top tranche is rated AAA, rock-solid, good as money.

If this seems too good to

be true to you, you're in good company. Guys like billionaire investor Warren

Buffet said the very logic was ridiculous. But back in 2005, 2006, the global

pool of money couldn't get enough of these things.

And the CDO industry was

facing the same pressures everyone else was at every other step of this chain.

To loosen their standards. To make CDOs out of lower and lower rated pools.

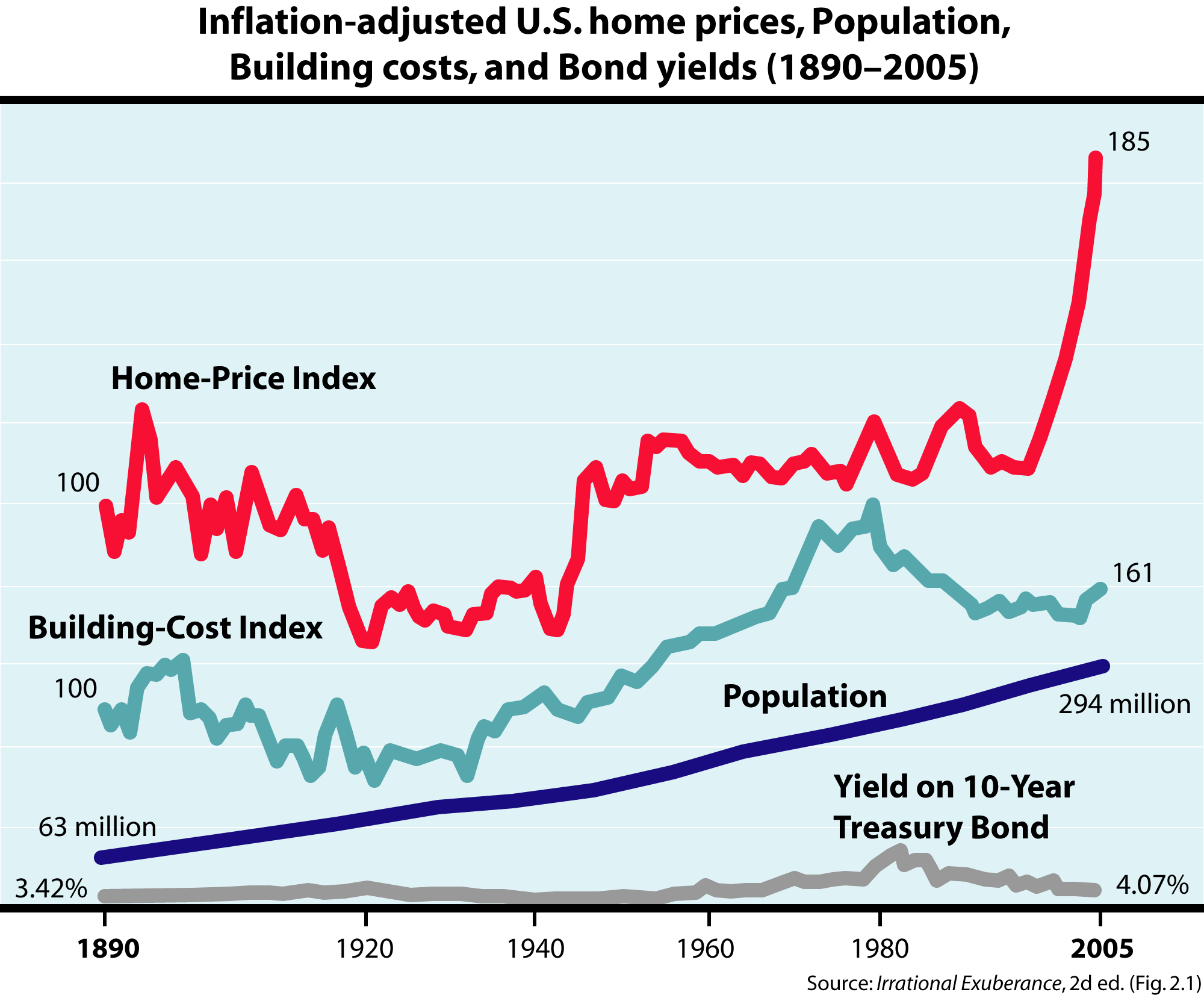

7 Bubble burst

The problem was that even

though housing prices were going through the roof, people weren't making any

more money. From 2000 to 2007, the median household income stayed flat. And so

the more prices rose, the more tenuous the whole thing became. No matter how

lax lending standards got, no matter how many exotic mortgage products were

created to shoehorn people into homes they couldn't possibly afford, no matter

what the mortgage machine tried, the people just couldn't swing it. By late

2006, the average home cost nearly four times what the average family made.

Historically it was between two and three times. And mortgage lenders noticed

something that they'd almost never seen before. People would close on a house,

sign all the mortgage papers, and then default on their very first payment. No

loss of a job, no medical emergency, they were underwater before they even

started. And although no one could really hear it, that was probably the moment

when one of the biggest speculative bubbles in American history popped.

Once property values

starting going down, it set off a reverse chain reaction, the opposite of what

had been happening in the bubble. As more people defaulted, more houses came on

the market. With no buyers, prices went even further down, and as prices

declined.

7.1 Late 2006. WallStreet stop

buying any mortgage from smaller local banks. Smaller banks borrowed from big

banks (like citi, Wamu) and pay them back when they sold the loan. Now that

they can't find any buyer, the smaller banks default

The way it worked was that

a small bank, like Silver State mortgage, where Mike Garner worked, would

borrow money from a big bank, say Citibank, or Washington Mutual. Silver State

would use this borrowed money to buy up a bunch of loans, and then pay back the

big bank once it sold the pools to Wall Street. Now these smaller banks were

highly leveraged, in most cases 20 to 1. Meaning,

in Silver state’s case, even though it only had 5 million of its own dollars,

it could borrow 20 times that, 100 million, to buy loans with. So in late 2006,

Mike is busily at it, borrowing, buying, selling, paying back, and borrowing

again, when the e-mails started coming:

Mike Garner: We’d get an

e-mail from a street firm, just say Credit Suisse/First Boston. It’d say, after

whatever date, “As of December 29th, we are no longer buying Stated Income with a FICO

less than whatever.” It’d say “There will be no exceptions. Pleas do not call

the pricing desk.” And you just start flipping out. Can't just say you're not

going to buy this with no notice. Well, we're saying it and there's no notice.

Then you start to scramble trying to get this stuff out of the door as soon as

you can.

Alex Blumberg: Because

you’ve already been assembling a bunch of those loans with those characteristics in place

somewhere.

Mike Garner: You've got 20

million sitting there, and you say oh crap, I better get those out the door.

Within a week, you can expect to see the same email from all them. A lot of

time you’ll get two of those the same day. You're scrambling to sell them,

going off sheer relationships. Like okay, I’ve still got 10 million of these. I

know you’re not buying them anymore. But come on ... you can't just leave me

like this. There comes a point where all of them said, we’re not buying

anything.

Alex Blumberg: For Mike and his company, that meant that they’d

borrowed tens of millions of dollars to buy loans, that now, they couldn’t

sell. And since they had very little of their own money, (just like the

homebuyers whose mortgages they’d purchased) they had no choice but to default

on their loan. Silver State Mortgage's nearly 600 employees were out of work.

Quite suddenly.

Mike Garner: It was

February 14th the email went out and said “Silver State

Mortgage might be going out of business, but we

think we can work something out so we’d encourage you to come in and work tomorrow

and give us one more day.” The next day, people came in and the e-mail went

out. “Unfortunately we were not able to work anything out. We’re closing our

doors today.” That's how most of these lenders go under. Everybody’s working

thinking everything’s great. Chugging along. All of the sudden, the bank says

you're done. People started grabbing their computers, copy machines, started

rolling them out the door. It was a mess. My thoughts were “Holy crap.

Everyone’s just stealing their stuff.”

Alex Blumberg: That

happened on Feb. 14th?

Mike Garner: Yup. My boss

calls it the valentine’s day massacre.”

8 Credit Crisis

A typical CDO factory owns

a share of 16 million homes. And each of those homes has lots of other owners --people

in other CDO offices around the world-- there are lots of them. You

start to see what a crazy web of confusing interconnections this whole process

is.

Most of AAA rated

mortgage-backed CDO's that the industry created since 2006, are now worth less

than half their value. Some are worth close to zero. But remember to all the

investment managers in the global pool of money who bought them, AAA meant safe

as government bonds. AAA was called a cash equivalent, money in the bank. It's

as if the global pool of money put trillions of dollars in a savings account,

came back one year later, and found out that half was gone.

The global pool of money

is avoiding anything with even the slightest hint of risk and that affects

everybody, no matter who you are. It's harder to borrow money to buy a house,

or build a factory, or bring your country boldly into the 21st century. Take

Iceland. A year ago it was easy for them to borrow billions. Now, they're seen

as too risky. Their central bank has to pay more than 15 percent interest get

anyone to loan them money. They could do better putting their national debt on

a credit card. Hungary, Kazakhstan, Turkey, are all in similar situations. You

might have heard about problems in student lending. Companies that needed

credit to survive are shutting down. The US expects more than 1.1 million

bankruptcies this year: twice the 2006 number.

This freezing of credit

all around the world is something new, the world has never seen anything on

this scale. When the crisis hit, last August, central bankers and finance

economists couldn't figure out how bad things might get. There was this

question people would ask: will things get like the 1930s or the 1970s? There

was real fear that, just like in the '30s, hundreds of banks would collapse,

there would be massive unemployment, there was talk of a new Great Depression.

That talk seems to have

faded and there's more talk that the next few years will feel like the 1970s.

There are lots of technical differences between this crisis and Jimmy Carter's

malaise. But for the average person, it could feel the same. It's not an

out-and-out depression. Everything's just kind of crappy. And not just in

housing or banking but for the economy as a whole. It’s barely growing. There

aren't a lot of new businesses, new jobs. Unemployment keeps creeping up. We're

just sort of stuck, in neutral, for a while.

Anyone under 45 probably

doesn't remember that 1970's malaise too well. Anyone under 30 has barely known

a US economy that wasn't growing. Now there's a decent chance we'll all get to

see what life felt like in the '70s, which isn't great.

It's pretty bad, actually,

unless you're comparing it to the 1930’s.