It's the end of the year so I could dare myself to do a little prediction for the next year.

As Charles Dickens used to say about London at the dusk of the Industrial Revolution, "it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us ...". Even the most epic economists don't know where things are going to be between Jan 2009 and Dec 2009.

That being said, I am actually more optimistic now than 6 month ago (before Dow lost 40% of its value). Why? because people in US are waking up and started reflecting on what damage consumerism has done to the nation. This leads to my 1st prediction:

Consumer index will drop while personal savings rate will go above 5% for the first time since 1995. This is considered disaster for the companies, because they can no longer generate revenue by selling things people don't really need. Advertisers would have a hard time persuading people that their life quality is measured by how much they spend and how many material goods they own. This leads to my 2nd prediction:

As the people depends less on large corporations and more on their own community, two-party politics will evolve into a balance of multiple forces (liberal, green parties taking more food hold) Republicans moving towards more progressive side and their right-wing conservative force becomes marginalized. This leads to my 3rd prediction:

US troops will withdraw from Iraq. No sensible government will put military adventures ahead of its own solvency. US will instead strengthen its bases in South Korean and Japan to fend off threats from North Korean and China. This leads to my 4th prediction:

China will use its economic muscle to form geo-political allies with Russia and South-east Asian countries and Pakistan. It will advance its nature resource claim in the South China sea, which might result in direct conflict with Japan. This leads to my 5th prediction:

China will have a direct trade war with US. EU will benefit by grabbing more market share in China. This will result in re-structuring of the WTO terms. This will turn the tide of globalization backwards. USD will lose its dominating power in world trade. This leads to my 6th prediction:

Major US companies will pull out its China operation due to government regulations and expiration of federal tax credits. This will boost employment in US and hurt profits of the big US corporations. The lower unemployment, shrinking demand for USD overseas and tightened supply from China will compound each other into a storm of inflation in the US. It will further surpress the real consumption in US. That is when I dump my shares of DBA.

So you might wonder what does technology plays there? Shouldn't the great innovation engine create more high margin "service" jobs and "green" jobs?

I don't know. It's really a wild card. I agree US has been the most efficient country when it comes to implementing and capitalizing innovations. But its creative sectors has long been dominated by people specialized in creating "financial product" (like CDO and CDS backed by subprime morgage ) rather than real product. Major pharmaceutical companies haven't deliver any successful new drugs for the last decade. Major IT companies haven't find any new killer applications that create real values for the last decade. With its economic strength weaks, the immigrates that helped them finding the "next big thing" will leave for their own home countries.

Wednesday, December 31, 2008

Tuesday, December 30, 2008

over-dramatization

In general, I agree with many of the premises (like materialism, phony Corporations, brainwashing success coaching, homosexual rights, gun control, real estate bubble) that the movie American Beauty is projecting. However, I have two complaints.

1) The movie touches so many issues without really explore the real reason behind any one of the them.

At the end of the movie, everything falls back to this zen like phony happiness state. So we should just all quit our job and trade weed? A 40 min NHK documentary would have been more informative.

2) The movie betrayed itself (or sold itself for box office success) by adding to much coincidences and dramatization. Maybe that's the only way it could survive Hollywood. Just like Revolutionary Road has to feature two stars from Titanic to draw enough attention.

1) The movie touches so many issues without really explore the real reason behind any one of the them.

At the end of the movie, everything falls back to this zen like phony happiness state. So we should just all quit our job and trade weed? A 40 min NHK documentary would have been more informative.

2) The movie betrayed itself (or sold itself for box office success) by adding to much coincidences and dramatization. Maybe that's the only way it could survive Hollywood. Just like Revolutionary Road has to feature two stars from Titanic to draw enough attention.

Thursday, December 25, 2008

Revolutionary Road

It's a new movie adapted from Ricard Yates 1950's novel.

Here is a wonderful review of the original novel. I am most touched by it because I share the same feeling watching the movie, finding myself mediocre and lacking: no better than anyone I used to look down at.

"

The American Dream, May 24, 2000

A good job, a pretty wife, nice kids, and a home in the suburbs. This

novel, written in 1961, is about a couple that lives this American

Dream. But this pre-yuppie pair leads a life of exquisite monotony. He

hates his white-collar job; she stays home with the kids. One of their

most frequent recreational activities is to visit with another similar

couple, and spend a few hours shaking their heads and complaining about

how unevolved everyone else is. We smile ruefully as we read about

them, thinking how common these folks are. Or have we fallen into a

trap by putting ourselves in the same place by looking down on Frank

and April as they look down on others.

Here is a wonderful review of the original novel. I am most touched by it because I share the same feeling watching the movie, finding myself mediocre and lacking: no better than anyone I used to look down at.

"

But Revolutionary Road was not what I expected from the reviews.

Yates knows all of the pitfalls of the standard send-up of the middle

class: the main characters in his story are not the usual suburban

types, but people who consider themselves better than the dull people

in their neighborhood; they mock the people that we, as readers, are so

used to mocking, and become our surrogates.

The real theme of

this book is much deeper, and it transcends the era and even the plot

of the book: what do people do when they are intelligent and spirited

enough not to be satisfied with the conformity and blandness of their

surroundings, but lack the drive to ever escape mediocrity, because

they are, fundamentally, much more a part of their environment than

they imagine?

The tragedy of this book is the discovery that you

are, after all, perhaps not as extraordinary as you thought - and that

has sting, because all of us, at some time, have thought that we were a

bit better than the people around us, and most of us have realized with

horror (although the realization doesn't always stick around) that we

aren't as different, as far above them, as we thought. Many of the

moments in this book stick with you because they remind you of those

moments when you came face to face with your own mediocrity, and

challenges you to either be honest with yourself about what you are, or

try sincerely to fulfill the ambitions that you have pursued so

halfheartedly until now.

It's a hard lesson to deal with: I can

tell why this book didn't sell. The writing, by the way, is beautiful;

scene after scene springs effortlessly to life, and you can't tell how

much skill is involved until you go back and read it again.

I

remember reading once that Yates - against the advice of his publishers

- called this book Revolutionary Road because it seemed to him that the

promise of the nation was petering out in the 50s, that the ambition

and hope that had marked its founding had slowly led to a dead-end of

uninspired and uninspiring prosperity (for some people, at least) -

that the end of the revolutionary road had been reached.

This is

overstated, and Yates's vision often seems to me unaccountably dark, as

if he was blind to everything but his thesis. Something about his

outlook is right, though; the problem with the society isn't

necessarily that it's hypocritical or conformist or mediocre, but that

it produces people with such a horrible gap between aspiration and

capacity - it gives them the leisure and intelligence to want a fuller

life while robbing them of the backbone to get it.

"

The American Dream, May 24, 2000

A good job, a pretty wife, nice kids, and a home in the suburbs. This

novel, written in 1961, is about a couple that lives this American

Dream. But this pre-yuppie pair leads a life of exquisite monotony. He

hates his white-collar job; she stays home with the kids. One of their

most frequent recreational activities is to visit with another similar

couple, and spend a few hours shaking their heads and complaining about

how unevolved everyone else is. We smile ruefully as we read about

them, thinking how common these folks are. Or have we fallen into a

trap by putting ourselves in the same place by looking down on Frank

and April as they look down on others.

Frank

and April Wheeler look forward to things: a part in a little theater

play, a move to Paris, an affair, a promotion. It would seem, though,

that for them happiness is only in the anticipation of events. The

story's participants also are deeply into playing roles with their

spouses, their co-workers, their friends, and above all with

themselves. There is no one in this book that you want to identify

with. Why? Is it because they are poor, hopelessly lost dullards, or is

it because they represent us in too many unpleasant ways? It's a sad

story, but one that makes you think about your own life, and the

ultimate value of what you have accomplished. While some of our culture

has changed since this book was written (we no longer sit in hospital

waiting rooms smoking cigarettes), its theme is as modern as can be.

art history of photography

This youtube playlist is BBC's 6 episode series "The Genius of Photography"

It rekindled my passion to imagery. The vast possibility of creating images that has a direct impact on the viewer.

I think Photosynth would someday be marked as an art form in the evolution of photography.

It rekindled my passion to imagery. The vast possibility of creating images that has a direct impact on the viewer.

I think Photosynth would someday be marked as an art form in the evolution of photography.

Tuesday, December 23, 2008

photosynth: Seattle spring, summer and autumn

Please follow this link to view it.

MSN space can't embed the iframe link generated by photosynth (kind of an irony).

MSN space can't embed the iframe link generated by photosynth (kind of an irony).

Wednesday, December 3, 2008

关于习惯

以前一直骑车上班,经过无数次轻重跌打损伤之后,我一个月没骑车了.这时候,我发现自己已经不是害怕跌倒,而是害怕骑车本身了.

今天给别人做code review, 我开始怀疑自己能否写出满足我所说的要求的code。我可以列一张长长的单子,写满我曾经视为习惯,但现在已经生疏的事(写blog就是其中之一)。

在过去的六个月中,我到底学会了哪些?放弃了哪些?荒废了哪些?

什么是我最需要坚持的习惯?

今天给别人做code review, 我开始怀疑自己能否写出满足我所说的要求的code。我可以列一张长长的单子,写满我曾经视为习惯,但现在已经生疏的事(写blog就是其中之一)。

在过去的六个月中,我到底学会了哪些?放弃了哪些?荒废了哪些?

什么是我最需要坚持的习惯?

Sunday, November 30, 2008

基督山伯爵

小时候看《基督山伯爵》,最痛快的是看到那些背叛朋友,陷害无辜的小人,获得应得的惩罚。

今天又看《基督山伯爵》,则想:如果艾德蒙有机会选择,他是否愿意成为基督山伯爵,一个为复仇而无情执行计划的人?

命运在他以为自己最幸运的时候为小人所害,囚禁伊夫堡;又在他最绝望的时候,使他重获新生,成为正义的化身。这是一种幸运,还是不幸?或许上帝的字典里,并没有“unfortunate”这个概念。

今天又看《基督山伯爵》,则想:如果艾德蒙有机会选择,他是否愿意成为基督山伯爵,一个为复仇而无情执行计划的人?

命运在他以为自己最幸运的时候为小人所害,囚禁伊夫堡;又在他最绝望的时候,使他重获新生,成为正义的化身。这是一种幸运,还是不幸?或许上帝的字典里,并没有“unfortunate”这个概念。

Saturday, November 29, 2008

如何穿透时代

《The man from Earth》触及一个最核心的问题:如果一个人能从远古活到今天,他会怎样生活?

事实上,用历史的眼光去看眼前的一切,就能和长生不老的人一样看透一切。今天的得失,在漫长的人生里,不过是沧海一粟,何足虑兮?

觉得《芙蓉镇》秦书田,能在扫大街的时候跳起华尔兹,就是到了这种境界,做到宠辱不惊,能随时享受生活中的快乐。

事实上,用历史的眼光去看眼前的一切,就能和长生不老的人一样看透一切。今天的得失,在漫长的人生里,不过是沧海一粟,何足虑兮?

觉得《芙蓉镇》秦书田,能在扫大街的时候跳起华尔兹,就是到了这种境界,做到宠辱不惊,能随时享受生活中的快乐。

Wednesday, November 5, 2008

being unreasonable

One of the feedback I got from those who reviews me is "need to concede that the world won't go according to his way." Lately, there are quite a few cases proves that true, so I was just about to admit that as my fault. Until I saw the following quote:

“The reasonable man adapts himself the the world; the

unreasonable one persists in trying to adapt the world to himself.

Therefore all progress depends on the unreasonable man.” - George Bernard Shaw

“As soon as we abandon our own reason, and are content to rely upon authority, there is no end to our troubles.” - Bertrand Russell

Anyway, we shouldn't act based on quotes, especially when those quotes are from a play-writer or a philosopher

Tuesday, October 21, 2008

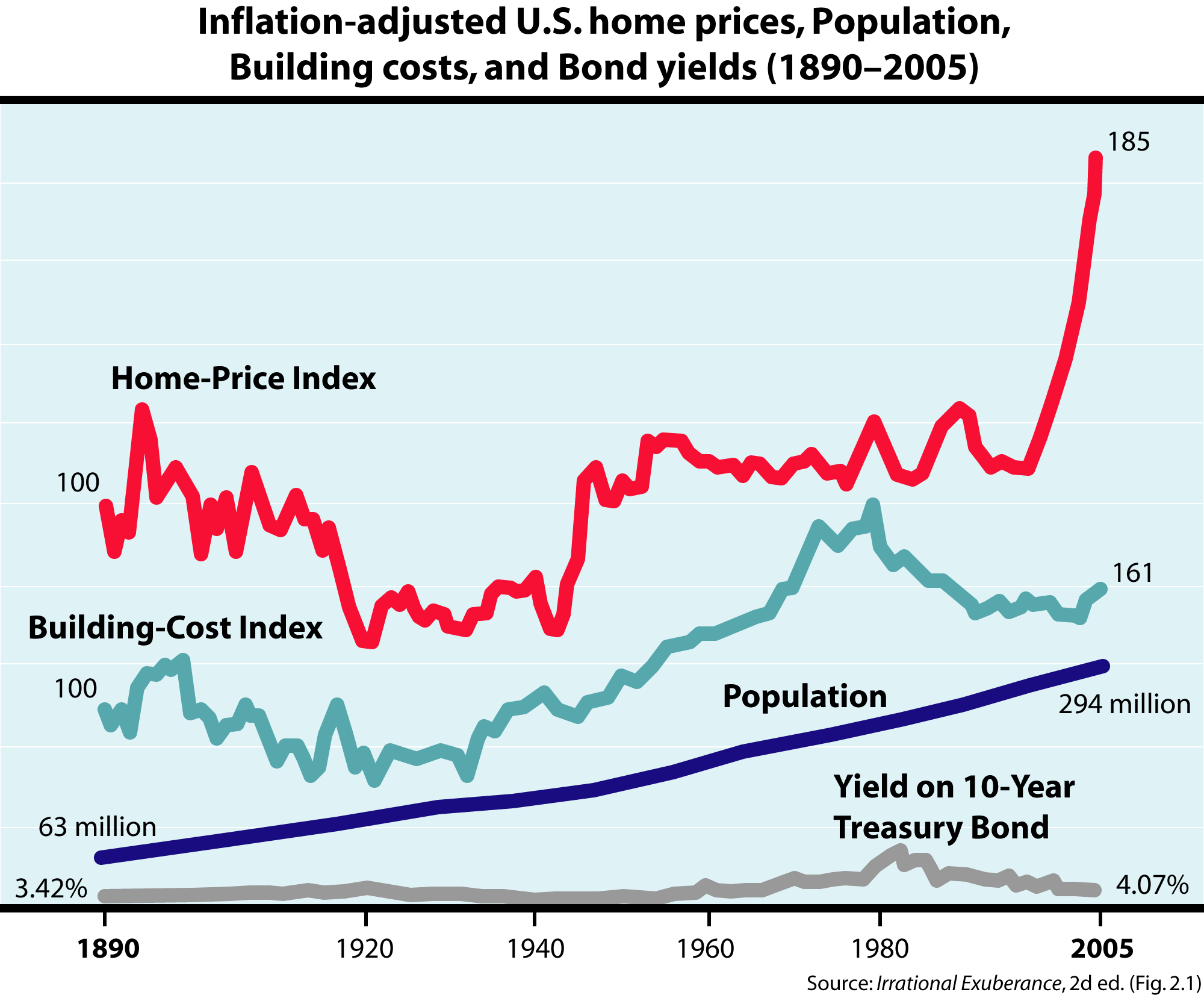

My 4th Toastmaster Speech: Life of a Bubble

Life of a Bubble: How did the global economic crisis

happen?

Key word: fed reserve, housing bubble, trade

deficit

1 Intro

Today I am going to talk about the life of a bubble. It's not just any bubble, it's the biggest one in the past 70 years if not the biggest one in human history. Most of the data came from US census, and the individual testimonies were excerpted from the

NPR special report on the credit crisis, originally aired on May 9, 2008

2 Global Pool of Money doubles

from 35 Trillion in 2001 to 70 Trillion 2007

2.1 Poor countrys getting rich

By making TVs and selling oil: China,

India, Saudi Arabia. Made a lot of money and banked it. China, for example, has

over a trillion dollars in its central bank, and there are office buildings in

Beijing filled with math geniuses-real math geniuses-looking for a place to

invest it. And the world was not ready for all this money. There's twice as

much money looking for investments, but there are not twice as many good

investments. So, that global army of investment managers was hungrier and

twitchier than ever before. They all wanted the same thing: a nice low risk

investment that paid some return.

Incidentally the US trade

deficit also doubled from 2001 to 2007

2001 -365.126 billion

2002 -423.725 billion

2003 -496.915 billion

2004 -607.730 billion

2005 -711.567 billion

2006 -753.283 billion

2007 -700.258 billion

2.2 Greenspan: Reduce The Fed

Funds Rate: From 6.6% in Jan 2001 to 1%

in July 2003

3 mortgage backed securities:

Mike Francis. During the beginning of the mortgage implosion, I was an

executive director at Morgan Stanley on the residential mortgage trading desk.

3.1 Think how attractive a

mortgage loan is to that 70 trillion dollar pool of money. Remember, they're

desperate to get any kind of interest return. They want to beat that miserable

1 percent interest Greenspan is offering them. And here are these homeowners,

they're paying 5, 7, 9 percent to borrow money from some bank. So what if the

global pool could get in on that action? There are problems. Individual

mortgages are too big a hassle for the global pool of money. They don't want

get mixed up with actual people and their catastrophic health problems or

debilitating divorces, and all the reasons which might stop them from paying

their mortgages.So what Mike and his peers on Wall Street did, was to figure

out how to give the global pool of money all the benefits of a mortgage –

basically higher yield - without the hassle or the risk. So picture the whole

chain. Home buyer gets a mortgage from a broker. The broker sells the mortgage

to a small bank, the small bank sells the mortgage to Mike in a big investment

firm on Wall Street. Then Mike takes a few thousand mortgages he’s bought this

way, he puts them in one big pile. Now he’s got thousands of mortgage checks

coming to him every month. It’s a huge monthly stream of money, which is

expected to come in for the next thirty years, the life of a mortgage. And he

then sells shares of that monthly income to investors. Those shares are called

mortgage backed securities. And the 70 trillion dollar global pool of money

loved them.

4 Drive the need for more

mortgage: lower the bar

And in the beginning, he'd

only buy mortgages that were pretty standard and pretty safe. Mortgages where

people had come up with a down payment and proven they had a steady income and

money in the bank.

And they sold so many

mortgages that there came a point in 2003 where just about

everybody who wanted a mortgage and was qualified

to get one .... had gotten one. But

the pool of money had just gotten started. They wanted more mortgage backed

securities.

So Wall Street had to find

more people to take out mortgages. Which meant lending

to people who never would’ve qualified before.

And so Mike noticed that

every month, the guidelines were getting a little looser.

Something called a stated income, verified asset

loan came out, which meant you didn't

have to provide paycheck stubs and w-2 forms, as they had in the past. You

could simply state your income, as long as you showed that you had money in the

bank.

Mike Garner: The next

guideline lower is just stated income, stated assets. Then you state what you

make and state what’s in your bank account.

They call and make sure

you work where you say you work. Then an accountant has to say for your field

it is possible to make what you said you make. But they don’t say what you

make, just say it’s possible that they could make that.

It’s just so funny that

instead of just asking people to prove what they make there’s this theater in place of you

have to find an accountant

sitting right in front of me who could very easily provide a W2, but we’re not

asking for a W2 form, but we do want this accountant to say yeah, what they’re

saying is plausible in some universe.

Loan officers would have

an accountant they could call up

and say “Can you write a statement saying a truck driver can make this much

money?” Then the next one, came along, and it was no income, verified assets.

So you don't have to tell the people what you do for a living. All you have to

do is state you have

a certain amount of money in your bank account. And then, the next one, is just

no income, no asset. You don't have to state anything. Just have to have a

credit score and a pulse.

Actually that pulse thing

is also optional. Like the case in Ohio where 23 dead people were approved for mortgages.

5 Housing bubble

It's easy to ignore your

gut fear when you are making a fortune in commissions. But Mike had other help in

rationalizing what he was doing.

Technological help. Mike

sat at a desk with six computer screens, connected to millions of dollars worth

of fancy analytic software designed by brilliant Ivy league math geniuses hired

by his firm, which analyzed all the loans in all the pools that he bought and

then sold. And the software, the data ... didn’t seem worried at all:

Mike Francis:

"All the data that we

had to review, to look at, on loans in production that were years old, was

positive. They performed very well. All those factors, when you look at the

pieces and parts. A 90% NINA loan from 3 years ago is performing amazingly

well. Has a little bit of risk. Instead of defaulting 1.5% of the time it

defaults at 3.5% of the time. That’s not so bad. If I’m an investor buying

that, if I get a little bit of return, I’m fine.

"

As we now know, they were

using the wrong data. They looked at the recent history of mortgages and saw

that foreclosure rate is generally below 2 percent. So they figured, absolute

worst-case scenario, the foreclosure rate may go to 8 or 10 or 12 percent. But

the problem with is there were all these new kinds of mortgages, given out to

people who never would have gotten them before. So the historical data was

irrelevant. Some mortgage pools, today, are expected to go beyond 50 percent

foreclosure rates.

That explains why the

mortgage backed security seems to perform well at the beginning of the bubble.

Why did it continue to perform will after the initial 3 years?

The answer is home equity

lines of credit, or HELOC.

Through HELOC, the home

owners could take out another loan from the bank, against the value of their

house, which had increased because of the bubble. HELOC became very popular

between 2003 and 2006, partly because they were easy to get; partly because

people needed them to continue making their original mortgage payments.

To pay off their debts,

they went into more debt.

5.1 A big part of this story,

of this whole crisis, is that a lot of really smart people, people who knew

better, fooled themselves with this data. It was the triumph of data over common

sense.

6 The thing that took this

problem and turned it into a crisis was something else that was new, something

called a Collateralized Debt Obligation, CDO

6.1 A mortgage-backed security,

you remember, is a pool of thousands of different mortgages. These are all put

together and divided into different slices. Some of these slices are risky,

some are not. OK, a CDO is a pool of those slices. A pool of pools.

There's another term the

industry uses, no joke, they call these lower-rated tranches toxic waste.

They're so high-risk, they're toxic.

So, a CDO is sort of a

financial alchemy. Jim takes that toxic stuff, these low- rated, high-risk

tranches, puts them all together. Re-tranches them, and presto: he has a CDO

whose top tranche is rated AAA, rock-solid, good as money.

If this seems too good to

be true to you, you're in good company. Guys like billionaire investor Warren

Buffet said the very logic was ridiculous. But back in 2005, 2006, the global

pool of money couldn't get enough of these things.

And the CDO industry was

facing the same pressures everyone else was at every other step of this chain.

To loosen their standards. To make CDOs out of lower and lower rated pools.

7 Bubble burst

The problem was that even

though housing prices were going through the roof, people weren't making any

more money. From 2000 to 2007, the median household income stayed flat. And so

the more prices rose, the more tenuous the whole thing became. No matter how

lax lending standards got, no matter how many exotic mortgage products were

created to shoehorn people into homes they couldn't possibly afford, no matter

what the mortgage machine tried, the people just couldn't swing it. By late

2006, the average home cost nearly four times what the average family made.

Historically it was between two and three times. And mortgage lenders noticed

something that they'd almost never seen before. People would close on a house,

sign all the mortgage papers, and then default on their very first payment. No

loss of a job, no medical emergency, they were underwater before they even

started. And although no one could really hear it, that was probably the moment

when one of the biggest speculative bubbles in American history popped.

Once property values

starting going down, it set off a reverse chain reaction, the opposite of what

had been happening in the bubble. As more people defaulted, more houses came on

the market. With no buyers, prices went even further down, and as prices

declined.

7.1 Late 2006. WallStreet stop

buying any mortgage from smaller local banks. Smaller banks borrowed from big

banks (like citi, Wamu) and pay them back when they sold the loan. Now that

they can't find any buyer, the smaller banks default

The way it worked was that

a small bank, like Silver State mortgage, where Mike Garner worked, would

borrow money from a big bank, say Citibank, or Washington Mutual. Silver State

would use this borrowed money to buy up a bunch of loans, and then pay back the

big bank once it sold the pools to Wall Street. Now these smaller banks were

highly leveraged, in most cases 20 to 1. Meaning,

in Silver state’s case, even though it only had 5 million of its own dollars,

it could borrow 20 times that, 100 million, to buy loans with. So in late 2006,

Mike is busily at it, borrowing, buying, selling, paying back, and borrowing

again, when the e-mails started coming:

Mike Garner: We’d get an

e-mail from a street firm, just say Credit Suisse/First Boston. It’d say, after

whatever date, “As of December 29th, we are no longer buying Stated Income with a FICO

less than whatever.” It’d say “There will be no exceptions. Pleas do not call

the pricing desk.” And you just start flipping out. Can't just say you're not

going to buy this with no notice. Well, we're saying it and there's no notice.

Then you start to scramble trying to get this stuff out of the door as soon as

you can.

Alex Blumberg: Because

you’ve already been assembling a bunch of those loans with those characteristics in place

somewhere.

Mike Garner: You've got 20

million sitting there, and you say oh crap, I better get those out the door.

Within a week, you can expect to see the same email from all them. A lot of

time you’ll get two of those the same day. You're scrambling to sell them,

going off sheer relationships. Like okay, I’ve still got 10 million of these. I

know you’re not buying them anymore. But come on ... you can't just leave me

like this. There comes a point where all of them said, we’re not buying

anything.

Alex Blumberg: For Mike and his company, that meant that they’d

borrowed tens of millions of dollars to buy loans, that now, they couldn’t

sell. And since they had very little of their own money, (just like the

homebuyers whose mortgages they’d purchased) they had no choice but to default

on their loan. Silver State Mortgage's nearly 600 employees were out of work.

Quite suddenly.

Mike Garner: It was

February 14th the email went out and said “Silver State

Mortgage might be going out of business, but we

think we can work something out so we’d encourage you to come in and work tomorrow

and give us one more day.” The next day, people came in and the e-mail went

out. “Unfortunately we were not able to work anything out. We’re closing our

doors today.” That's how most of these lenders go under. Everybody’s working

thinking everything’s great. Chugging along. All of the sudden, the bank says

you're done. People started grabbing their computers, copy machines, started

rolling them out the door. It was a mess. My thoughts were “Holy crap.

Everyone’s just stealing their stuff.”

Alex Blumberg: That

happened on Feb. 14th?

Mike Garner: Yup. My boss

calls it the valentine’s day massacre.”

8 Credit Crisis

A typical CDO factory owns

a share of 16 million homes. And each of those homes has lots of other owners --people

in other CDO offices around the world-- there are lots of them. You

start to see what a crazy web of confusing interconnections this whole process

is.

Most of AAA rated

mortgage-backed CDO's that the industry created since 2006, are now worth less

than half their value. Some are worth close to zero. But remember to all the

investment managers in the global pool of money who bought them, AAA meant safe

as government bonds. AAA was called a cash equivalent, money in the bank. It's

as if the global pool of money put trillions of dollars in a savings account,

came back one year later, and found out that half was gone.

The global pool of money

is avoiding anything with even the slightest hint of risk and that affects

everybody, no matter who you are. It's harder to borrow money to buy a house,

or build a factory, or bring your country boldly into the 21st century. Take

Iceland. A year ago it was easy for them to borrow billions. Now, they're seen

as too risky. Their central bank has to pay more than 15 percent interest get

anyone to loan them money. They could do better putting their national debt on

a credit card. Hungary, Kazakhstan, Turkey, are all in similar situations. You

might have heard about problems in student lending. Companies that needed

credit to survive are shutting down. The US expects more than 1.1 million

bankruptcies this year: twice the 2006 number.

This freezing of credit

all around the world is something new, the world has never seen anything on

this scale. When the crisis hit, last August, central bankers and finance

economists couldn't figure out how bad things might get. There was this

question people would ask: will things get like the 1930s or the 1970s? There

was real fear that, just like in the '30s, hundreds of banks would collapse,

there would be massive unemployment, there was talk of a new Great Depression.

That talk seems to have

faded and there's more talk that the next few years will feel like the 1970s.

There are lots of technical differences between this crisis and Jimmy Carter's

malaise. But for the average person, it could feel the same. It's not an

out-and-out depression. Everything's just kind of crappy. And not just in

housing or banking but for the economy as a whole. It’s barely growing. There

aren't a lot of new businesses, new jobs. Unemployment keeps creeping up. We're

just sort of stuck, in neutral, for a while.

Anyone under 45 probably

doesn't remember that 1970's malaise too well. Anyone under 30 has barely known

a US economy that wasn't growing. Now there's a decent chance we'll all get to

see what life felt like in the '70s, which isn't great.

It's pretty bad, actually,

unless you're comparing it to the 1930’s.

Sunday, October 19, 2008

Perfect Storm for Bankers with Government connection: read Goldman Sachs

The Guys From ‘Government Sachs’

Photo illustration by The New York Times

Treasury faces, from left: Steve Shafran (formerly of Goldman),

Kendrick Wilson III (ditto), Henry Paulson Jr. (you guessed it), Edward

Forst (yep) and Neel Kashkari (see a trend?).

By JULIE CRESWELL and BEN WHITE

Published: October 17, 2008

THIS summer, when the Treasury secretary, Henry M. Paulson Jr., sought help navigating the Wall Street meltdown, he turned to his old firm, Goldman Sachs, snagging a handful of former bankers and other experts in corporate restructurings.

Robert Rubin, right, an ex-Goldman co-chairman and a

Treasury secretary in the Clinton administration, promoted Timothy F.

Geithner at Treasury. Mr. Geithner now leads the New York Fed.

Treasury secretary in the Clinton administration, promoted Timothy F.

Geithner at Treasury. Mr. Geithner now leads the New York Fed.

From top: Win McNamee/Getty Images; Dennis Brack/Bloomberg News; Jay Mallin/Bloomberg News

Joshua B. Bolten, top, a former Goldman executive, is President Bush’s

chief of staff. Stephen Friedman, a former chairman of Goldman, is

chairman of the New York Fed. This fall, as part of its bailout, the

government put Edward M. Liddy, then a Goldman director, in charge of

A.I.G.

In September, after the government bailed out the American International Group, the faltering insurance giant, for $85 billion, Mr. Paulson helped select a director from Goldman’s own board to lead A.I.G.

And earlier this month, when Mr. Paulson needed someone to oversee the government’s proposed $700 billion bailout

fund, he again recruited someone with a Goldman pedigree, giving the

post to a 35-year-old former investment banker who, before coming to

the Treasury Department, had little background in housing finance.

Indeed, Goldman’s presence in the department and around the federal response to the financial crisis is so ubiquitous that other bankers and competitors have given the star-studded firm a new nickname: Government Sachs.

The

power and influence that Goldman wields at the nexus of politics and

finance is no accident. Long regarded as the savviest and most admired

firm among the ranks — now decimated — of Wall Street investment banks,

it has a history and culture of encouraging its partners to take

leadership roles in public service.

It is a widely held view

within the bank that no matter how much money you pile up, you are not

a true Goldman star until you make your mark in the political sphere.

While Goldman sees this as little more than giving back to the

financial world, outside executives and analysts wonder about potential

conflicts of interest presented by the firm’s unique perch.

They

note that decisions that Mr. Paulson and other Goldman alumni make at

Treasury directly affect the firm’s own fortunes. They also question

why Goldman, which with other firms may have helped fuel the financial

crisis through the use of exotic securities, has such a strong hand in

trying to resolve the problem.

The very scale of the financial

calamity and the historic government response to it have spawned a host

of other questions about Goldman’s role.

Analysts wonder why

Mr. Paulson hasn’t hired more individuals from other banks to limit the

appearance that the Treasury Department has become a de facto Goldman

division. Others ask whose interests Mr. Paulson and his coterie of

former Goldman executives have in mind: those overseeing tottering

financial services firms, or average homeowners squeezed by the crisis?

Still others question whether Goldman alumni leading the federal

bailout have the breadth and depth of experience needed to tackle

financial problems of such complexity — and whether Mr. Paulson has

cast his net widely enough to ensure that innovative responses are

pursued.

“He’s brought on people who have the same life

experiences and ideologies as he does,” said William K. Black, an

associate professor of law and economics at the University of Missouri and counsel to the Federal Home Loan Bank Board during the savings and loan

crisis of the 1980s. “These people were trained by Paulson, evaluated

by Paulson so their mind-set is not just shaped in generalized group

think — it’s specific Paulson group think.”

Not so fast, say

Goldman’s supporters. They vehemently dismiss suggestions that Mr.

Paulson’s team would elevate Goldman’s interests above those of other

banks, homeowners and taxpayers. Such chatter, they say, is a paranoid

theory peddled, almost always anonymously, by less successful rivals.

Just add black helicopters, they joke.

“There is no conspiracy,” said Donald C. Langevoort, a law professor at Georgetown University.

“Clearly if time were not a problem, you would have a committee of

independent people vetting all of the potential conflicts, responding

to questions whether someone ought to be involved with a particular

aspect or project or not because of relationships with a former firm —

but those things do take time and can’t be imposed in an emergency

situation.”

In fact, Goldman’s admirers say, the firm’s ranks should be praised, not criticized, for taking a leadership role in the crisis.

“There

are people at Goldman Sachs making no money, living at hotels, trying

to save the financial world,” said Jes Staley, the head of JPMorgan Chase’s asset management division. “To indict Goldman Sachs for the people helping out Washington is wrong.”

Goldman

concurs. “We’re proud of our alumni, but frankly, when they work in the

public sector, their presence is more of a negative than a positive for

us in terms of winning business,” said Lucas Van Praag, a spokesman for

Goldman. “There is no mileage for them in giving Goldman Sachs the

corporate equivalent of most-favored-nation status.”

MR. PAULSON himself landed atop Treasury because of a Goldman tie. Joshua B. Bolten, a former Goldman executive and President Bush’s chief of staff, helped recruit him to the post in 2006.

Some

analysts say that given the pressures Mr. Paulson faced creating a SWAT

team to address the financial crisis, it was only natural for him to

turn to his former firm for a capable battery.

And if there is

one thing Goldman has, it is an imposing army of top-of-their-class,

up-before-dawn über-achievers. The most prominent former Goldman banker

now working for Mr. Paulson at Treasury is also perhaps the most

unlikely.

Neel T. Kashkari

arrived in Washington in 2006 after spending two years as a low-level

technology investment banker for Goldman in San Francisco, where he

advised start-up computer security companies. Before joining Goldman,

Mr. Kashkari, who has two engineering degrees in addition to an M.B.A.

from the Wharton School of the University of Pennsylvania, worked on

satellite projects for TRW, the space company that now belongs to

Northrop Grumman.

He was originally appointed to oversee a $700

billion fund that Mr. Paulson orchestrated to buy toxic and complex

bank assets, but the role evolved as his boss decided to invest

taxpayer money directly in troubled financial institutions.

Mr.

Kashkari, who met Mr. Paulson only briefly before going to the Treasury

Department, is also in charge of selecting the staff to run the bailout

program. One of his early picks was Reuben Jeffrey, a former Goldman

executive, to serve as interim chief investment officer.

Mr.

Kashkari is considered highly intelligent and talented. He has also

been Mr. Paulson’s right-hand man — and constant public shadow — during

the financial crisis.

He played a main role in the emergency sale of Bear Stearns

to JPMorgan Chase in March, sitting in a Park Avenue conference room as

details of the acquisition were hammered out. He often exited the room

to funnel information to Mr. Paulson about the progress.

Despite

Mr. Kashkari’s talents in deal-making, there are widespread questions

about whether he has the experience or expertise to manage such a

project.

“Mr. Kashkari may be the most brilliant, talented

person in the United States, but the optics of putting a 35-year-old

Paulson protégé in charge of what, at least at one point, was supposed

to be the most important part of the recovery effort are just very

damaging,” said Michael Greenberger, a University of Maryland law professor and a former senior official with the Commodity Futures Trading Commission.

“The

American people are fed up with Wall Street, and there are plenty of

people around who could have been brought in here to offer broader

judgment on these problems,” Mr. Greenberger added. “All wisdom about

financial matters does not reside on Wall Street.”

Mr. Kashkari

won’t directly manage the bailout fund. More than 200 firms submitted

bids to oversee pieces of the program, and Treasury has winnowed the

list to fewer than 10 and could announce the results as early as this

week. Goldman submitted a bid but offered to provide its services

gratis.

While Mr. Kashkari is playing a prominent public role, other Goldman alumni dominate Mr. Paulson’s inner sanctum.

The

A-team includes Dan Jester, a former strategic officer for Goldman who

has been involved in most of Treasury’s recent initiatives, especially

the government takeover of the mortgage giants Fannie Mae and Freddie Mac. Mr. Jester has also been central to the effort to inject capital into banks, a list that includes Goldman.

Another

central player is Steve Shafran, who grew close to Mr. Paulson in the

1990s while working in Goldman’s private equity business in Asia.

Initially focused on student loan problems, Mr. Shafran quickly became involved in Treasury’s initiative to guarantee money market funds, among other things.

Mr.

Shafran, who retired from Goldman in 2000, had settled with his family

in Ketchum, Idaho, where he joined the city council. Baird Gourlay, the

council president, said he had spoken a couple of times with Mr.

Shafran since he returned to Washington last year.

“He was

initially working on the student loan part of the problem,” Mr. Gourlay

said. “But as things started falling apart, he said Paulson was relying

on him more and more.”

The Treasury Department said Mr. Shafran and the other former Goldman executives were unavailable for comment.

Other

prominent former Goldman executives now at Treasury include Kendrick R.

Wilson III, a seasoned adviser to chief executives of the nation’s

biggest banks. Mr. Wilson, an unpaid adviser, mainly spends his time

working his ample contact list of bank chiefs to apprise them of

possible Treasury plans and gauge reaction.

Another Goldman

veteran, Edward C. Forst, served briefly as an adviser to Mr. Paulson

on setting up the bailout fund but has since left to return to his post

as executive vice president of Harvard.

Robert K. Steel, a former vice chairman at Goldman, was tapped to look

at ways to shore up Fannie Mae and Freddie Mac. Mr. Steel left Treasury

to become chief executive of Wachovia this summer before the government took over the entities.

Treasury

officials acknowledge that former Goldman executives have played an

enormous role in responding to the current crisis. But they also note

that many other top Treasury Department officials with no ties to

Goldman are doing significant work, often without notice. This group

includes David G. Nason, a senior adviser to Mr. Paulson and a former

Securities and Exchange Commission official.

Robert F. Hoyt,

general counsel at Treasury, has also worked around the clock in recent

weeks to make sure the department’s unprecedented moves pass legal

muster. Michele Davis is a Capitol Hill veteran and Treasury policy

director. None of them are Goldmanites.

“Secretary Paulson has

a deep bench of seasoned financial policy experts with varied

experience,” said Jennifer Zuccarelli, a spokeswoman for the Treasury.

“Bringing additional expertise to bear at times like these is clearly

in the taxpayers’ and the U.S. economy’s best interests.”

While

many Wall Streeters have made the trek to Washington, there is no

question that the axis of power at the Treasury Department tilts toward

Goldman. That has led some to assume that the interests of the bank,

and Wall Street more broadly, are the first priority. There is also the

question of whether the department’s actions benefit the personal

finances of the former Goldman executives and their friends.

“To the extent that they have a portfolio or blind trust that holds Goldman Sachs stock, they have conflicts,” said James K. Galbraith, a professor of government and business relations at the University of Texas.

“To the extent that they have ties and alumni loyalty or friendships

with people that are still there, they have potential conflicts.”

Mr.

Paulson, Mr. Kashkari and Mr. Shafran no longer own any Goldman shares.

It is unclear whether Mr. Jester or Mr. Wilson does because, according

to the Treasury Department, they were hired as contractors and are not

required to disclose their financial holdings.

For every

naysayer, meanwhile, there is also a Goldman defender who says the

bank’s alumni are doing what they have done since the days when Sidney

Weinberg ran the bank in the 1930s and urged his bankers to give

generously to charities and volunteer for public service.

“I give

Hank credit for attracting so many talented people. None of these guys

need to do this,” said Barry Volpert, a managing director at Crestview

Partners and a former co-chief operating officer of Goldman’s private

equity business. “They’re not getting paid. They’re killing themselves.

They haven’t seen their families for months. The idea that there’s some

sort of cabal or conflict here is nonsense.”

In fact, say some

Goldman executives, the perception of a conflict of interest has

actually cost them opportunities in the crisis. For instance, Goldman

wasn’t allowed to examine the books of Bear Stearns when regulators

were orchestrating an emergency sale of the faltering investment bank.

THIS summer, as he fought for the survival of Lehman Brothers, Richard S. Fuld Jr.,

its chief executive, made a final plea to regulators to turn his

investment bank into a bank holding company, which would allow it to

receive constant access to federal funding.

Timothy F. Geithner, the president of the Federal Reserve Bank of New York,

told him no, according to a former Lehman executive who requested

anonymity because of continuing investigations of the firm’s demise.

Its options exhausted, Lehman filed for bankruptcy in mid-September.

One week later, Goldman and Morgan Stanley were designated bank holding companies.

“That

was our idea three months ago, and they wouldn’t let us do it,” said a

former senior Lehman executive who requested anonymity because he was

not authorized to comment publicly. “But when Goldman got in trouble,

they did it right away. No one could believe it.”

The New York

Fed, which declined to comment, has become, after Treasury, the

favorite target for Goldman conspiracy theorists. As the most powerful

regional member of the Federal Reserve

system, and based in the nation’s financial capital, it has been a

driving force in efforts to shore up the flailing financial system.

Mr.

Geithner, 47, played a pivotal role in the decision to let Lehman die

and to bail out A.I.G. A 20-year public servant, he has never worked in

the financial sector. Some analysts say that has left him reliant on

Wall Street chiefs to guide his thinking and that Goldman alumni have

figured prominently in his ascent.

After working at the New York

consulting firm Kissinger Associates, Mr. Geithner landed at the

Treasury Department in 1988, eventually catching the eye of Robert E. Rubin,

Goldman’s former co-chairman. Mr. Rubin, who became Treasury secretary

in 1995, kept Mr. Geithner at his side through several international

meltdowns, including the Russian credit crisis in the late 1990s.

Mr. Rubin, now senior counselor at Citigroup, declined to comment.

A

few years later, in 2003, Mr. Geithner was named president of the New

York Fed. Leading the search committee was Pete G. Peterson, the former

head of Lehman Brothers and the senior chairman of the private equity

firm Blackstone. Among those on an outside advisory committee were the

former Fed chairman Paul A. Volcker; the former A.I.G. chief executive Maurice R. Greenberg; and John C. Whitehead, a former co-chairman of Goldman.

The

board of the New York Fed is led by Stephen Friedman, a former chairman

of Goldman. He is a “Class C” director, meaning that he was appointed

by the board to represent the public.

Mr. Friedman, who wears

many hats, including that of chairman of the President’s Foreign

Intelligence Advisory Board, did not return calls for comment.

During

his tenure, Mr. Geithner has turned to Goldman in filling important

positions or to handle special projects. He hired a former Goldman

economist, William C. Dudley, to oversee the New York Fed unit that

buys and sells government securities. He also tapped E. Gerald

Corrigan, a well-regarded Goldman managing director and former New York

Fed president, to reconvene a group to analyze risk on Wall Street.

Some

people say that all of these Goldman ties to the New York Fed are

simply too close for comfort. “It’s grotesque,” said Christopher

Whalen, a managing partner at Institutional Risk Analytics and a critic

of the Fed. “And it’s done without apology.”

A person familiar

with Mr. Geithner’s thinking who was not authorized to speak publicly

said that there was “no secret handshake” between the New York Fed and

Goldman, describing such speculation as a conspiracy theory.

Furthermore, others say, it makes sense that Goldman would have a presence in organizations like the New York Fed.

“This

is a very small, close-knit world. The fact that all of the major

financial services firms, investment banking firms are in New York City

means that when work is to be done, you’re going to be dealing with one

of these guys,” said Mr. Langevoort at Georgetown. “The work of

selecting the head of the New York Fed or a blue-ribbon commission —

any of that sort of work — is going to involve a standard cast of

characters.”

Being inside may not curry special favor anyway,

some people note. Even though Mr. Fuld served on the board of the New

York Fed, his proximity to federal power didn’t spare Lehman from

bankruptcy.

But when bankruptcy loomed for A.I.G. — a collapse

regulators feared would take down the entire financial system — federal

officials found themselves once again turning to someone who had a

Goldman connection. Once the government decided to grant A.I.G., the

largest insurance company, an $85 billion lifeline (which has since

grown to about $122 billion) to prevent a collapse, regulators,

including Mr. Paulson and Mr. Geithner, wanted new executive blood at

the top.

They picked Edward M. Liddy, the former C.E.O. of the insurer Allstate.

Mr. Liddy had been a Goldman director since 2003 — he resigned after

taking the A.I.G. job — and was chairman of the audit committee.

(Another former Goldman executive, Suzanne Nora Johnson, was named to

the A.I.G. board this summer.)

Like many Wall Street firms,

Goldman also had financial ties to A.I.G. It was the insurer’s largest

trading partner, with exposure to $20 billion in credit derivatives,

and could have faced losses had A.I.G. collapsed. Goldman has said

repeatedly that its exposure to A.I.G. was “immaterial” and that the

$20 billion was hedged so completely that it would have insulated the

firm from significant losses.

As the financial crisis has taken

on a more global cast in recent weeks, Mr. Paulson has sat across the

table from former Goldman colleagues, including Robert B. Zoellick, now president of the World Bank;

Mario Draghi, president of the international group of regulators called

the Financial Stability Forum; and Mark J. Carney, the governor of the

Bank of Canada.

BUT Mr. Paulson’s home team is still what draws the most scrutiny.

“Paulson

put Goldman people into these positions at Treasury because these are

the people he knows and there are no constraints on him not to do so,”

Mr. Whalen says. “The appearance of conflict of interest is everywhere,

and that used to be enough. However, we’ve decided to dispense with the

basic principles of checks and balances and our ethical standards in

times of crisis.”

Ultimately, analysts say, the actions of Mr. Paulson and his alumni club may come under more study.“I

suspect the conduct of Goldman Sachs and other bankers in the rescue

will be a background theme, if not a highlighted theme, as Congress

decides how much regulation, how much control and frankly, how punitive

to be with respect to the financial services industry,” said Mr.

Langevoort at Georgetown. “The settling up is going to come in Congress

next spring.”

Saturday, October 18, 2008

Why a long recession is good for Microsoft

1) Credit crunch will weed out a lot of startup that provide "free" software/service, because they needs to generate positive cashflow sooner than they had planned.

2) Weak economy will tighten the advertising budgets, therefore hurting Google's cashcow. Google will have to cutback on its investment in challenging MS's desktop applications.

3) Weak economy will push Yahoo over the edge and into MS's arms at a much lower cost than MS was originally planning to pay.

4) MS is sitting on a lot of cash, which is a becoming more and more scare resource. They have more leverage in buying out competition or launching campaigns against its competitors (read Apple).

5) With high unemployment, MS can find the much needed talent they wouldn't have seen on the market during booming years.

2) Weak economy will tighten the advertising budgets, therefore hurting Google's cashcow. Google will have to cutback on its investment in challenging MS's desktop applications.

3) Weak economy will push Yahoo over the edge and into MS's arms at a much lower cost than MS was originally planning to pay.

4) MS is sitting on a lot of cash, which is a becoming more and more scare resource. They have more leverage in buying out competition or launching campaigns against its competitors (read Apple).

5) With high unemployment, MS can find the much needed talent they wouldn't have seen on the market during booming years.

Wednesday, October 15, 2008

Why Corporate American is rotten to the core

A typical US corporation raises its funding by selling a worthless shell to the public through IB. Those banks that died in the last four weeks because they oversold mortgage-backed securities (The word "security" itself is an irony, because there is really nothing secure about those and other "securities").

Since IPO, the management team struggles to make up the "numbers" to show to "the Street". They make up the numbers by investing most the cash flow into marketing (aka advertising) so that people will buy things they don't need; by openning sweatshop all over the world, by privatizing natural resource that belongs to the planet.

What does "the management team" made up of? First there are board of directors (including chairman, president, CEO, big investors, outside directors). They represents the ultramate power. They can oust a CEO with enough votes. Under CEO, there is CFO, COO, CTO/CIO.

CFO is in charge of cooking the book, therefore are paid the most. He controls the budget, therefore has the most direct power. CTO/CIO is only considered a cost for plumbing "the computers".

In some public company, the president, the chairman of BOD, the largest shareholder, the CEO are the same person. Such company is very easy to be ruled as a totalitrian regime.

In other cases, where the CEO is a "professional" excutive, but not a big shareholder. The CEO will focus even more on short-term profit, which is directly linked to his bonus. By the time he screws up the company too much he will leave with a huge pension and severance package.

Examples are:

Henry Paulson (Goldman Sachs $600 million)

Robert Nardelli (Home Depot $225 million)

Michael Ovitz (Disney $140 million)

Stephen Hilbert (Conseco $72 million)

Carly Fiorina (HP $42 million)

Gary Forsee (Sprint $40-million-plus)

Charles Prince (Citigroup, $40 million)

Angelo Mozilo (Countrywide, $100 million)

Kerry Killinger (WaMu $20 million)

Martin Sullivan (AIG $47 million)

Stan O'Neal (Merrill Lynch $160 million in stock).

If we do a simple math (which the CFOs loves to do), the severance packages listed above already amounts to $1.486 billion, and that's a very incompletely list.

When the same trend spreads to Europe: Gerard Le Fur (Sanofi Aventis

$9.51 million), we had to laugh at the large

scale of anger among the French public, because that's really just a fraction of Gerard's US counterparts are getting.

If there were a Capitalist Manifesto, those names should be the underwriters.

After reading all this, will you still be surprised that we are in a recession? Will you still doubt about Henry Paulson's determination to bail-out the banks including Goldman Sachs with $700 billion of taxpayer money?

Since IPO, the management team struggles to make up the "numbers" to show to "the Street". They make up the numbers by investing most the cash flow into marketing (aka advertising) so that people will buy things they don't need; by openning sweatshop all over the world, by privatizing natural resource that belongs to the planet.

What does "the management team" made up of? First there are board of directors (including chairman, president, CEO, big investors, outside directors). They represents the ultramate power. They can oust a CEO with enough votes. Under CEO, there is CFO, COO, CTO/CIO.

CFO is in charge of cooking the book, therefore are paid the most. He controls the budget, therefore has the most direct power. CTO/CIO is only considered a cost for plumbing "the computers".

In some public company, the president, the chairman of BOD, the largest shareholder, the CEO are the same person. Such company is very easy to be ruled as a totalitrian regime.

In other cases, where the CEO is a "professional" excutive, but not a big shareholder. The CEO will focus even more on short-term profit, which is directly linked to his bonus. By the time he screws up the company too much he will leave with a huge pension and severance package.

Examples are:

Henry Paulson (Goldman Sachs $600 million)

Robert Nardelli (Home Depot $225 million)

Michael Ovitz (Disney $140 million)

Stephen Hilbert (Conseco $72 million)

Carly Fiorina (HP $42 million)

Gary Forsee (Sprint $40-million-plus)

Charles Prince (Citigroup, $40 million)

Angelo Mozilo (Countrywide, $100 million)

Kerry Killinger (WaMu $20 million)

Martin Sullivan (AIG $47 million)

Stan O'Neal (Merrill Lynch $160 million in stock).

If we do a simple math (which the CFOs loves to do), the severance packages listed above already amounts to $1.486 billion, and that's a very incompletely list.

When the same trend spreads to Europe: Gerard Le Fur (Sanofi Aventis

$9.51 million), we had to laugh at the large

scale of anger among the French public, because that's really just a fraction of Gerard's US counterparts are getting.

If there were a Capitalist Manifesto, those names should be the underwriters.

After reading all this, will you still be surprised that we are in a recession? Will you still doubt about Henry Paulson's determination to bail-out the banks including Goldman Sachs with $700 billion of taxpayer money?

Shit goes downhill

The problem with top-down management is that it exposes the tiniest flaw of the upper management.

For example, when the CEO disrespects SVP and micromanaging them with fear and intimation, the same behavior will be transmitted down the chain of command and magnifies to the whole company scale.

Those very few in the middle management that knows better will suffer both ways and leave as soon as the stock option vested.

Another example is hypocrisy in performance review and promotion.When the economy is going down, there is less need to motivate the employee with promotion or raise. Everybody expects that. But instead be frank about it, the whole chain of management uses excuses like "lack of cross-team collaboration" (which is implicitly discouraged) to make the review looks like the employee is incompetent. This kind of hypocrisy is just unethical and unprofessional.

For example, when the CEO disrespects SVP and micromanaging them with fear and intimation, the same behavior will be transmitted down the chain of command and magnifies to the whole company scale.

Those very few in the middle management that knows better will suffer both ways and leave as soon as the stock option vested.

Another example is hypocrisy in performance review and promotion.When the economy is going down, there is less need to motivate the employee with promotion or raise. Everybody expects that. But instead be frank about it, the whole chain of management uses excuses like "lack of cross-team collaboration" (which is implicitly discouraged) to make the review looks like the employee is incompetent. This kind of hypocrisy is just unethical and unprofessional.

Friday, October 3, 2008

How to demonstrate leadership

Leadership is about doing the right thing (most of the time). But practicing leadership is not enough. Branding yourself as a leader is just as important if not more.

And here is how:

Todo:

Focus: you don't have the right to fail. It impacts your brand.

Confidence: do your homework before any conversation

IQ and expertise gets you in the door. EQ (human quality) makes you success.

Understand your audience (who has different background and point of view)

Straight line may not be the shortest distance.

Most organizations are political instead of logical and rational. Efficiency is not always the goal. People have different goals.

Decision makers act based more on past emotional experiences than logic.

Don't communicate when you are upset

Report talk instead of rapport talk

Use I "believe" instead of I "feel"

Always ask a question within 5 minutes of a meeting: You have to get involved

Cut people off when necessary, otherwise you will never be heard

Hope and Fear are what move people. You need to use BOTH.

Power is good. Always ask for more money and stuff when you can.

It's critical to rise above being a information source and technologist.

______________________________________________________________

Disclaimer:

The content above is based on Atefeh Biazi's keynote speech at Emtech 2008 hosted by MIT Technology Review.

If you want to watch the video, you can skip the first 10 minutes (they recorded 10 minutes of background music before the talk started).

My Comment:

It almost feels like what Chinese culture has taught us needs to be undone.

Thursday, October 2, 2008

Wednesday, October 1, 2008

How company culture can affect people's vision

Today I saw bunch of engineers from an major desktop software company discussing how their desktop PC is being upgraded to quad-core.

I felt very amused, because I happened to be checking my team's infrastructure capacity. What I notice is that our average production server is 16 times faster than my desktop with 8 times more memory.

And the challenge my team faces is how to migrate our software across hosts without bringing down the service, not how fast any individual machine runs.

To be fair, the performance of an individual host still matters, but it's becoming less relevant when our software can be easily deployed to 100 hosts and scale up 100 times, without waiting for Intel or AMD to add more cores.

As I said some time ago, the failing of Moore's law has given CS people an exciting new frontier. If a company is not facing up to the new reality, its days are counted.

I felt very amused, because I happened to be checking my team's infrastructure capacity. What I notice is that our average production server is 16 times faster than my desktop with 8 times more memory.

And the challenge my team faces is how to migrate our software across hosts without bringing down the service, not how fast any individual machine runs.

To be fair, the performance of an individual host still matters, but it's becoming less relevant when our software can be easily deployed to 100 hosts and scale up 100 times, without waiting for Intel or AMD to add more cores.

As I said some time ago, the failing of Moore's law has given CS people an exciting new frontier. If a company is not facing up to the new reality, its days are counted.

Tuesday, September 30, 2008

My 3rd Toastmaster speech (Project 3 Get to the Point)

Title of My Speech: How many of you would like to cut down your living expense?

General purpose: inform the audience on ways to cut down living expense

Specific purpose:

After hearing my speech, the audience should have a list of action items that they can followup in their daily life to cut down living expenses.

Illustration on the board:

I draw a pie marked income and split it into two sections expense and saving. Using the pie chart, I illustrated to boost savings, you need to reduce expenses.

I also listed the 3 steps and 5 categories on the side. They serve as the take-home message for the audience as well as my own cheat-sheet.

__________________________________________________________________________________________

Below is the body of my script. I skipped some of them and improvised some on the fly (like the anecdote of Lehman Brother chairman Richard Fuld selling his modern art collections to make extra income.)

__________________________________________________________________________________________

Raise your hand if you think you would like to have more savings and less debt.

OK, I see quite a few of you are interested in the topic. Today I am going to share with you the 3 steps to increase your saving by cutting-back on unnecessary expenditures.

Step 1) Tracking

Use a budget spreadsheet to record how much money you spend on everything, from mortgage/rent payment to groceries. From car insurance to miscellaneous spending. Putting down those records will give you a clear picture of where you money went.

Step 2) Examining

Going through the spreadsheet to determine what is necessary and what is not.

Most people's list can be divided into the following 5 categories.

1. Food and beverage

Make your own coffee in the morning to avoid spending a dollar to two dollars a day on the way to work, which amount to $50 a month. Cooking your own meal and taking your own lunch to work can save you $400 a month. Staying away from vending machines can save you up to $60 a month.

Buy nonperishable groceries like coffee and tea on special, in bulk. Buy generic brand instead of attach to a brand. Look for items on sale. Buy fruit and vegetable in season.

Alcohol can be a major drain on the household economy. No suggestion that you eliminate it altogether, but consider cutting back.

2. Transportation

Fuel is one of the growing expenses on our day to day lives. Limiting the fuel that we use is a priority. Plan your journeys to include everything that you need. Avoid unnecessary repeat trips to the shops and rediscover the joy of walking. Learn how to drive more economically, and make sure that your tires are inflated correctly. Learn to service your car yourself. Consider exchanging the fuel guzzling vehicle for a more economical model. Moving closer to work can save you commute time and fuel.

3. Utility

Heating and electricity bill can be very high in winter.Turn the thermometer down and wear more clothing at home. Make sure there are no leaks around windows and doors.

Health inspector say washing dishes in cold water is as effective as in hot water, so you can save heating expense by using cold water. If you are using dishwasher, you can safely lower the water heater temperature to 110 to 115 degree and stop the dishwasher before it hits the dry cycle. Shutdown the dishwasher and open the door will let the dishes dry faster.

Switch off whatever you are not using, including lights and computers. Swap your light bulb to energy efficient equivalents can save you 90% of the electricity. Put a brick in your toilet will save you a litre of water per flush.

If you are using high-speed internet, consider sharing the service with a neighbor.

Cut out or downgrade your cable TV. Borrow movies from the library instead of renting.

4. Impulse buy

Before buying a particular item, always ask yourself: Is the item something you want rather than need. If you really need the product, then the purchase can be justified. Be careful of what you put into your shopping cart, make a list before you come to the store, and then committing to the list while shopping. It not only makes your shopping more efficient, but keeps you from overspending.

Don't go grocery shopping while you're hungry. You'll end up thinking everything looks good and buy more than you need. Be careful with membership warehouse stores, researchers show that Costco and Sam's club membership make you buy more than you need.

5. Rent/mortgage payment

If all those small savings are still not enough, consider changing your accommodations. Move to a cheaper area.

Step 3) Budgeting

After examing the 5 categories, decide how much you would spend in each category per month. Minus that from your monthly income, you will find how much you can save each month. Put that money away at the beginning of each month.

If you are short on money at the end of the month, you know you are over-spending and need to adjust the budget next month.

Finally, I would like to close my speech by encouraging everyone to follow the 3 steps. It can make real difference on your own bottom line.

General purpose: inform the audience on ways to cut down living expense

Specific purpose:

After hearing my speech, the audience should have a list of action items that they can followup in their daily life to cut down living expenses.

Illustration on the board:

I draw a pie marked income and split it into two sections expense and saving. Using the pie chart, I illustrated to boost savings, you need to reduce expenses.

I also listed the 3 steps and 5 categories on the side. They serve as the take-home message for the audience as well as my own cheat-sheet.

__________________________________________________________________________________________

Below is the body of my script. I skipped some of them and improvised some on the fly (like the anecdote of Lehman Brother chairman Richard Fuld selling his modern art collections to make extra income.)

__________________________________________________________________________________________

Raise your hand if you think you would like to have more savings and less debt.

OK, I see quite a few of you are interested in the topic. Today I am going to share with you the 3 steps to increase your saving by cutting-back on unnecessary expenditures.

Step 1) Tracking

Use a budget spreadsheet to record how much money you spend on everything, from mortgage/rent payment to groceries. From car insurance to miscellaneous spending. Putting down those records will give you a clear picture of where you money went.

Step 2) Examining

Going through the spreadsheet to determine what is necessary and what is not.

Most people's list can be divided into the following 5 categories.

1. Food and beverage

Make your own coffee in the morning to avoid spending a dollar to two dollars a day on the way to work, which amount to $50 a month. Cooking your own meal and taking your own lunch to work can save you $400 a month. Staying away from vending machines can save you up to $60 a month.

Buy nonperishable groceries like coffee and tea on special, in bulk. Buy generic brand instead of attach to a brand. Look for items on sale. Buy fruit and vegetable in season.

Alcohol can be a major drain on the household economy. No suggestion that you eliminate it altogether, but consider cutting back.

2. Transportation

Fuel is one of the growing expenses on our day to day lives. Limiting the fuel that we use is a priority. Plan your journeys to include everything that you need. Avoid unnecessary repeat trips to the shops and rediscover the joy of walking. Learn how to drive more economically, and make sure that your tires are inflated correctly. Learn to service your car yourself. Consider exchanging the fuel guzzling vehicle for a more economical model. Moving closer to work can save you commute time and fuel.

3. Utility

Heating and electricity bill can be very high in winter.Turn the thermometer down and wear more clothing at home. Make sure there are no leaks around windows and doors.

Health inspector say washing dishes in cold water is as effective as in hot water, so you can save heating expense by using cold water. If you are using dishwasher, you can safely lower the water heater temperature to 110 to 115 degree and stop the dishwasher before it hits the dry cycle. Shutdown the dishwasher and open the door will let the dishes dry faster.

Switch off whatever you are not using, including lights and computers. Swap your light bulb to energy efficient equivalents can save you 90% of the electricity. Put a brick in your toilet will save you a litre of water per flush.

If you are using high-speed internet, consider sharing the service with a neighbor.

Cut out or downgrade your cable TV. Borrow movies from the library instead of renting.

4. Impulse buy

Before buying a particular item, always ask yourself: Is the item something you want rather than need. If you really need the product, then the purchase can be justified. Be careful of what you put into your shopping cart, make a list before you come to the store, and then committing to the list while shopping. It not only makes your shopping more efficient, but keeps you from overspending.

Don't go grocery shopping while you're hungry. You'll end up thinking everything looks good and buy more than you need. Be careful with membership warehouse stores, researchers show that Costco and Sam's club membership make you buy more than you need.

5. Rent/mortgage payment

If all those small savings are still not enough, consider changing your accommodations. Move to a cheaper area.

Step 3) Budgeting

After examing the 5 categories, decide how much you would spend in each category per month. Minus that from your monthly income, you will find how much you can save each month. Put that money away at the beginning of each month.

If you are short on money at the end of the month, you know you are over-spending and need to adjust the budget next month.

Finally, I would like to close my speech by encouraging everyone to follow the 3 steps. It can make real difference on your own bottom line.

Friday, September 26, 2008

Bailout and Excutive Power

Since the Bush Administration took office in 2000, they have been playing the same trick again and again.

The basic plot is:

Mess up big time,

Use fear and panic to manipulate the media and general public,

Ask for a blank check from congress,

Spend taxpayer money for their own benefit.

This weekend, we will see the bailout plan following the same route. The rich and powerful lawmakers sitting in their million-dollar water-front house will vote on whether to use poor tax payers' money to pay for their mortgage and their CEO friend's red-ink.

The basic plot is:

Mess up big time,

Use fear and panic to manipulate the media and general public,

Ask for a blank check from congress,

Spend taxpayer money for their own benefit.

This weekend, we will see the bailout plan following the same route. The rich and powerful lawmakers sitting in their million-dollar water-front house will vote on whether to use poor tax payers' money to pay for their mortgage and their CEO friend's red-ink.

Wednesday, September 17, 2008

5D Mark II

HD video quality is great. Storage card would be a bottleneck if anyone want to use it for serious film production.

But the concept is great, one day Canon will ship a DSLR with built-in hard drive.

But the concept is great, one day Canon will ship a DSLR with built-in hard drive.

Management vs Leadership

Excerpts from this weeks I, Cringely . The Pulpit | PBS

"Management is telling people what to do, which is a vital part of any

industrial economy. Leadership is figuring out what ought to be done

then getting people to do it, which is very different."

"Modern corporations suffer from systemic-level issues that emerge in

top-down hierarchies. Managers are there to control staff and budgets,

not to lead. Although you can make valiant and often successful

attempts to control things and processes, you will never again be able

to control people. We've evolved, basically, and the information age

has had a lot to do with it. So we still "manage" companies the same

way as when we actually operated assembly lines in America--the good

old days! Now, people need leaders, not managers, and that's what a

fractal organization enables.

"Management is telling people what to do, which is a vital part of any

industrial economy. Leadership is figuring out what ought to be done